Why a DSCR2 Loan Could Be the Solution You've Been Searching For

DSCR (Debt Service Coverage Ratio) loans have been tailored to assist both novice and experienced real estate investors in acquiring properties and expanding their portfolios. Unlike traditional loans, DSCR loans do not require proof of personal income. Instead, eligibility hinges on the property's cash flow, resulting in quicker approvals and more adaptable funding options. Continue reading to explore the advantages and disadvantages of DSCR loans to determine if they align with your next real estate investment opportunity.

What Is the Debt Service Coverage Ratio (DSCR)?

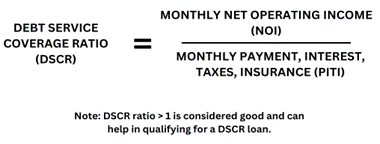

The Debt Service Coverage Ratio, or DSCR for short, is like a measuring stick that banks and lenders use to see if you can repay a loan. Here's why it matters for real estate investors: When you do your taxes, you often take deductions to lower your taxable income. But this can make it hard to get a regular loan because the bank sees your income as lower than it is. So, they might say no. But DSCR loans are different. They look at the money your property makes, like the rent you collect, instead of just your personal income or job history.

You can figure out your DSCR by dividing your properties rental income by your PITI amount. This gives you a number that shows if your property's income is enough to cover the loan. If it is, it's easier to get a loan.

How Do DSCR Loans Work?

DSCR loans are specifically meant for investors, not for buying a primary home. Instead, they're for purchasing or refinancing long term rental properties, like houses, apartments, condos, or townhomes. DSCR loans help lenders figure out if you can pay back the loan using the money you make from renting out your property. They use the DSCR calculation to measure this. If your DSCR is 1, it means the rental income is just enough to pay the loan, but that's not typically enough for a lender to consider funding the loan. There are other expenses like repairs and employees than can impact the DSCR. So, most lenders want to see a higher DSCR, usually at least 1.20 to qualify. This shows that you can cover the loan and still have some extra money for those other expenses. Having a higher DSCR makes lenders more likely to give you a bigger loan and at better rates. Even though lenders don't look at your personal income, they will still need to verify the property can earn enough income to justify the loan. To apply for these loans, you'll need to provide a lease agreement that shows how much rent you're collecting and get an appraisal of the property to confirm value. Not having a signed lease agreement in force can sometimes mean higher interest rates because of the additional risk assumed by the lender.

Advantages of DSCR Loans:

Accessibility: DSCR loans are simpler to qualify for because they don't require your personal income or job history. This makes them available to various borrowers, including both new and experienced investors.

Lower Interest Rates: DSCR loans usually have significantly lower interest rates than hard money loans.

Streamlined Approval Process: DSCR loans often have a quicker application and approval process compared to other types of investment loans. Since personal financial information isn't needed, the process is straightforward, leading to faster approvals and closing times.

Cash Out Up To 75% LTV: These loans allow you to take out money to fund your next deal.

No Property Limit: DSCR loans enable investors to purchase multiple properties simultaneously. Unlike traditional loans, where you typically need to pay off your existing debt before buying another property, DSCR loans let you expand your portfolio without such restrictions.

ersatile Property Types: DSCR loans can be used for various rental property types, including short and long-term rentals, single and multi-family homes.

Risks of DSCR Loans:

Limited Financing: DSCR loans typically range from a minimum of $150,000 to a maximum of $5,000,000. If you're purchasing multiple properties or a high-value property in an expensive market, these loans might not suffice.

For Rentals Only: DSCR loans are exclusively for non-owner-occupied rental properties and cannot be used for primary residences or house-flipping projects. They must be used for properties that generate rental income.

Vacancy Concerns: Rental properties may experience vacancies from time to time, which can impact your cash flow. Lenders don't usually consider your ability to repay the mortgage during vacancies, potentially leading to increased debt if consistent cash flow isn't maintained.

Get Started With a DSCR Loan

Bench Equity, LLC has partnered with some of the nations leading DSCR lenders to offer you the most competitive rates. Get started today by contacting us at (480) 222-5844 or sending an email to info@benchequity.com. We're ready to help you take advantage of the great possibilities DSCR loans have to offer!